TL; DR

- Ecommerce businesses have access to fast and flexible financing options like credit lines, merchant cash advances, and crowdfunding, but choosing the right one requires careful evaluation.

- Ecommerce financing gives you the flexibility to scale, handle cash flow issues, or prepare for seasonal sales, but plan carefully to ensure it works for you, not against you.

- Pick the right option based on your business goals to avoid unnecessary costs or repayment headaches. Be mindful of hidden fees, repayment terms, and the impact on control of your business, especially with equity-based financing.

A few years ago, ecommerce sellers who needed extra funds had two options—traditional bank loans or help from friends and family. But both came with limits. Bank loans had rigid terms and long approval times, while personal support only went so far.

Today, new funding models understand the realities of running an online store.

Instead of going through weeks of paperwork and waiting, you can apply online in minutes. Approval is based on real-time sales data from platforms like Amazon, TikTok Shop, Shopify, Lazada, Shopee, or other relevant marketplaces, not just credit scores or collateral.

That means if your store is doing well, you’re more likely to get funded quickly.

But not all financing is created equal. With more options now available—credit lines, merchant cash advances (MCAs), overdrafts—it’s easy to get overwhelmed. And picking the wrong one slows you down, eats into profits, complicates repayments, and squeezes your cash flow when you need it most.

In this post, we’ll break down 8 ecommerce financing options and help you find the one that fits your business stage, sales model, and goals, so you get the funds without the stress.

Signs Your Store Is Ready for Funding

Not every cash crunch means you should rush to take a loan.

Sometimes, financing gives your ecommerce business the breathing space it needs — but at other times, it leads to more stress than support.

Here’s how to tell the difference:

1. Upcoming sales or seasonal spikes

If you’re gearing up for a big sale season, like Amazon Prime Day, TikTok Deals For You, the Great Singapore Sale or the 11.11 sale, short-term financing helps you stock up on inventory, prepare your warehouse, or run pre-sale ads without draining your working capital.

Since revenue is likely to rise soon, you’ll also be better positioned to repay the loan on time.

2. Slow operating cycle

Some ecommerce categories — like furniture, made-to-order items, or high-value electronics — naturally take longer from production to delivery to getting paid.

If your business has a slow operating cycle, financing helps bridge that gap. It ensures that even while you’re waiting on one batch, you can keep production going or restock faster. This, in return, helps you fulfill orders and maintain customer trust without stalling your business.

3. Delayed payouts blocking cash flow

If you’re selling on marketplaces like Amazon, TikTok Shop, eBay, Shopify, payouts come with a delay. That means you’ve already shipped the item, but your working capital is stuck.

Short-term financing (like invoice or debtor financing) helps you access a percentage of that blocked amount early. You get stuck cash without waiting weeks, helping you reinvest in ads, inventory, or logistics in real time.

When to Avoid Taking Ecommerce Financing

Just because a lender is willing to give you money doesn’t mean you should take it.

Here are a few times when holding off is the smarter move:

1. When terms are unfavorable

If a loan comes with high interest, rigid daily repayments (like Merchant Cash Advance or MCAs), or hidden charges — it’s best to pause.

Some lenders market “quick loans” that seem tempting but pile on fees later or lock you into strict repayment schedules, even if your sales dip.

Instead of easing cash flow, it adds pressure, especially if you’re already running tight. You end up paying more than you gain.

2. When cash flow is unstable or unpredictable

If your sales are erratic or you’re not confident about your revenue in the coming weeks, borrowing could dig you into a deeper hole.

Without a reliable repayment plan, you risk defaulting, hurting both your creditworthiness and peace of mind.

If you’re not sure how or when you’ll repay, it’s better to wait and stabilize your income first.

Ecommerce Financing Options That Support Your Growth

Not all loans or credit options are the same.

Whether you’re looking for short-term relief or planning to scale, there are various types of financing available.

Here are 8 popular funding solutions, along with who they’re best for and when to consider them.

Note: This serves as a guide, and terms may be different across lending providers.

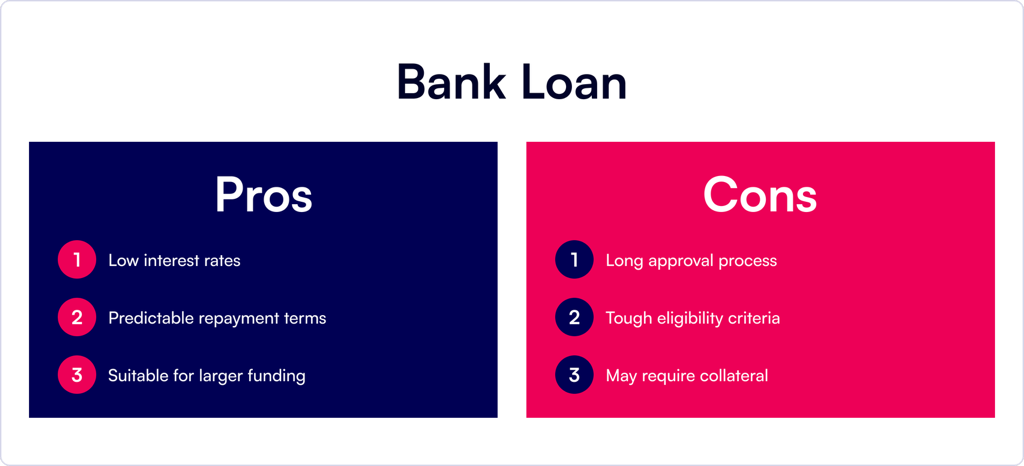

1. Bank Loan

A traditional loan from a bank, where a fixed sum is lent upfront and repaid over time with interest. Typically involves detailed paperwork and longer approval times.

General Eligibility:

- Registered business (1–2+ years)

- Good credit score (650+)

- Solid revenue and profitability

- Collateral may be required

2. Bank Overdraft

An overdraft lets you withdraw more money than you have in your account, up to a pre-approved limit. You only pay interest on the amount you use.

General Eligibility:

- Business current account (with history)

- Stable monthly bank activity

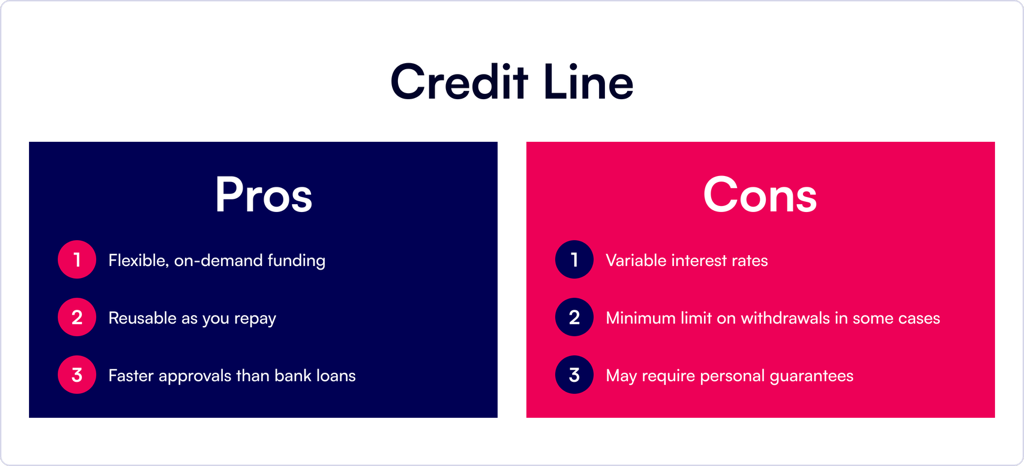

3. Credit Line

A revolving line of credit that you can dip into when needed. Interest is charged only on the amount used, and you can reuse the credit as you repay.

General Eligibility:

- Strong revenue: Typically, at least $100,000 in annual sales

- Good credit history: A credit score of 650 or higher

- Some lenders accept early-stage businesses

- Consistent repayment performance

4. Merchant Cash Advance (MCA)

Lump-sum cash given in exchange for a percentage of your future sales. Repaid automatically through card sales or bank debits daily/weekly.

General Eligibility:

- Minimum annual revenue: Around $120,000 or more

- Monthly credit card sales: At least $5,000

- Business operating for at least 6 months

- No strict credit score requirements, but lenders may prefer a score of 500+

- Steady sales history and consistent cash flow

- Gateway or point of sale (POS) integration

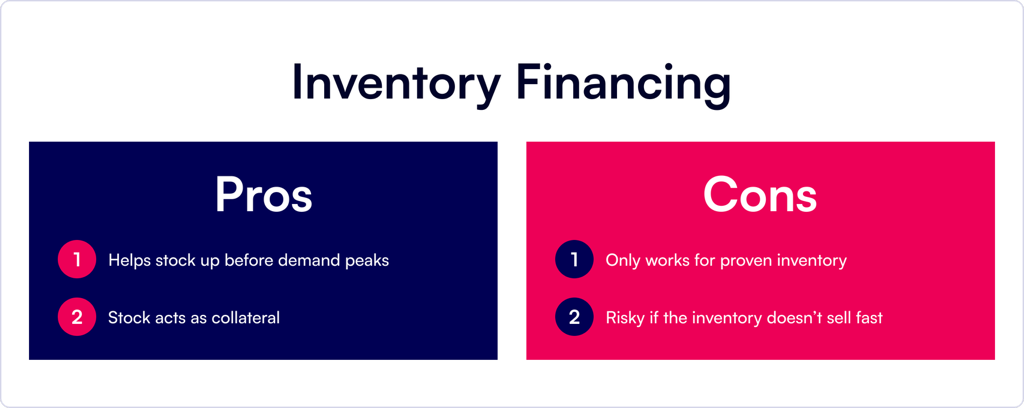

5. Inventory Financing

A loan or credit given specifically to buy inventory. The inventory itself acts as collateral, and repayment is tied to product turnover.

General Eligibility:

- Annual Revenue: $100,000 to $250,000+

- Business History: At least 6–12 months in business

- Inventory Value: $300,000+ in inventory

- Credit Score: 550+

- Proven, fast-moving SKUs

- Reliable supplier network

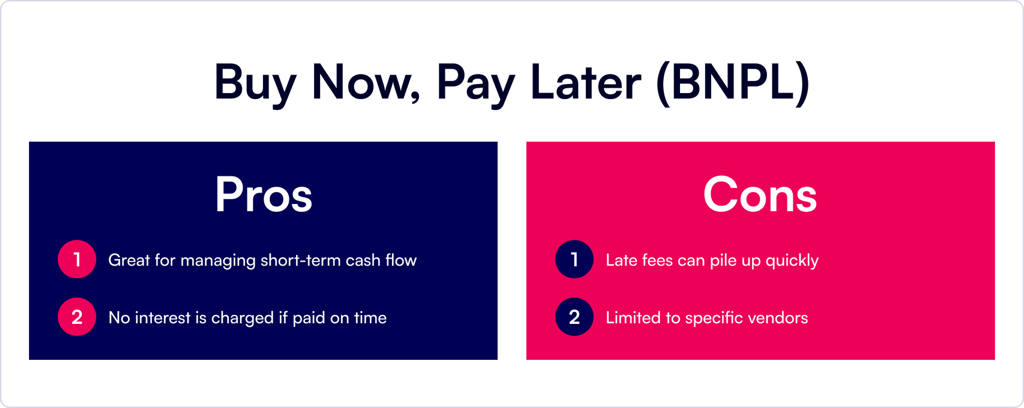

6. Buy Now, Pay Later (BNPL)

“Buy Now, Pay Later” solutions let you purchase goods/services now and pay in installments later, usually interest-free if paid on time.

General Eligibility:

- Annual Revenue: $50,000 to $500,000+

- Business History: 6+ months in operation

- Credit check may apply

- Stable sales with consistent growth

- Approved vendors or marketplaces

7. Angel Investors

High-net-worth individuals invest in your business in exchange for equity (ownership). They may also provide mentorship or strategic support.

General Eligibility:

- High-growth or scalable business idea

- Strong founding team

8. Crowdfunding

Raise funds by pitching your product idea or business to the public via online platforms like Kickstarter or Indiegogo. Backers contribute small amounts in return for rewards, early access, or shares.

General Eligibility:

- Strong product story or cause

- Time and skill to create a campaign

- Community or social media presence

Picking the Right Ecommerce Funding Option Based on Your Goal

Different business needs call for different financing choices.

Here’s a simple way to match your business goal with the right funding option.

Red Flags to Watch Out for in Ecommerce Financing

At times, ecommerce financing instead of funding the growth leads to deeper debt, reduced profits, and limited flexibility.

In this section, we’ll outline the key pitfalls to watch out for when securing funding for your business.

1. Hidden fees

Some funding options come with fees that aren’t obvious at first—processing charges, maintenance fees, early repayment penalties, or platform charges. These add up fast and eat into your profits.

Always read the fine print and ask for a clear breakdown of all costs involved. Compare multiple lenders to ensure transparency.

2. Tricky repayment structure

Some financing options have complex repayment structures that make it hard to predict your cash flow.

For example, daily repayments, interest-only periods, or fluctuating rates lead to confusion and financial stress.

Choose financing options with clear, predictable terms. Understand how payments work, whether it’s fixed or flexible, and how it aligns with your sales cycle.

3. Equity dilution

Equity financing, like angel investment, requires you to give up a portion of your business. While this brings in capital, it also means losing some control and a share of profits long-term.

Assess how much control you’re willing to give up.

Don’t agree to terms that put you in a position where your equity stake is significantly reduced unless necessary.

4. Planning usage

Securing a line of credit or loan is easy, but without a clear plan for how to use the funds, it quickly leads to overspending or mismanagement, putting you back in a worse financial position.

Create a sales forecast or financial plan to know exactly how much funding you need and how it will be used.

Always aim for a strategic, rather than reactive, approach.

5. Annual percentage rate (APR)

Annual percentage rate (APR) gives the actual yearly cost of the funds, including fees and interest. Some lenders advertise low “rates” but skip the full APR—making offers look cheaper than they are.

Compare APRs across different financing options to ensure you’re getting the best deal.

6. Backup plan for repayment

Delays in payouts or a dip in sales mess up your repayment ability.

Without a backup source—like reserve funds, insurance, or a contingency plan—you risk defaulting or hurting your credit score, making future funding harder.

Flexible Financing That Works at Your Pace

Ecommerce moves fast.

A delay in accessing funds means missing out on the very opportunity you were gearing up for—whether it’s a high-traffic sales event, a bulk inventory deal, or scaling your ad budget in time.

But financing doesn’t have to slow you down.

The right solution adapts to your business stage, supports your cash flow, and gets you funded without the weeks-long wait or confusing terms.

Whether you’re launching, scaling, or just getting through a cash crunch—better funding options are out there.